Flax-Linen and Hemp Economic Observatory

The Alliance has set up its economic observatory to collect, develop and share reliable data and information on European Flax and Hemp production. Providing decisionmaking tools: an overview of global markets, regulatory monitoring, barometer, weak signal analysis and dedicated economic studies.

Summary

-

European flax fibre market in 2026

> May 22, 2026 - Information release Q2 2026

> January 30, 2026 - Information release Q1 2026

> Key Production Figures for European Flax Fibre - 2026 - European hemp fibre production

- Previous flax and hemp information releases

European flax fibre market in 2026

July 30, 2026 - Information release Q3 2026

- Update to be published

May 22, 2026 - Information release Q2 2026

2026 Harvest: A favourable start to the season and a new record in surface area

- Spring Flax planting was completed by mid-April in most growing regions. The weather conditions for sowing were favourable.

- The month of April was particularly dry, resulting in limited levels of rainfall on seedlings. Although the situation does not pose a threat to the hectares that have been planted, future growth will depend on weather conditions in the coming weeks.

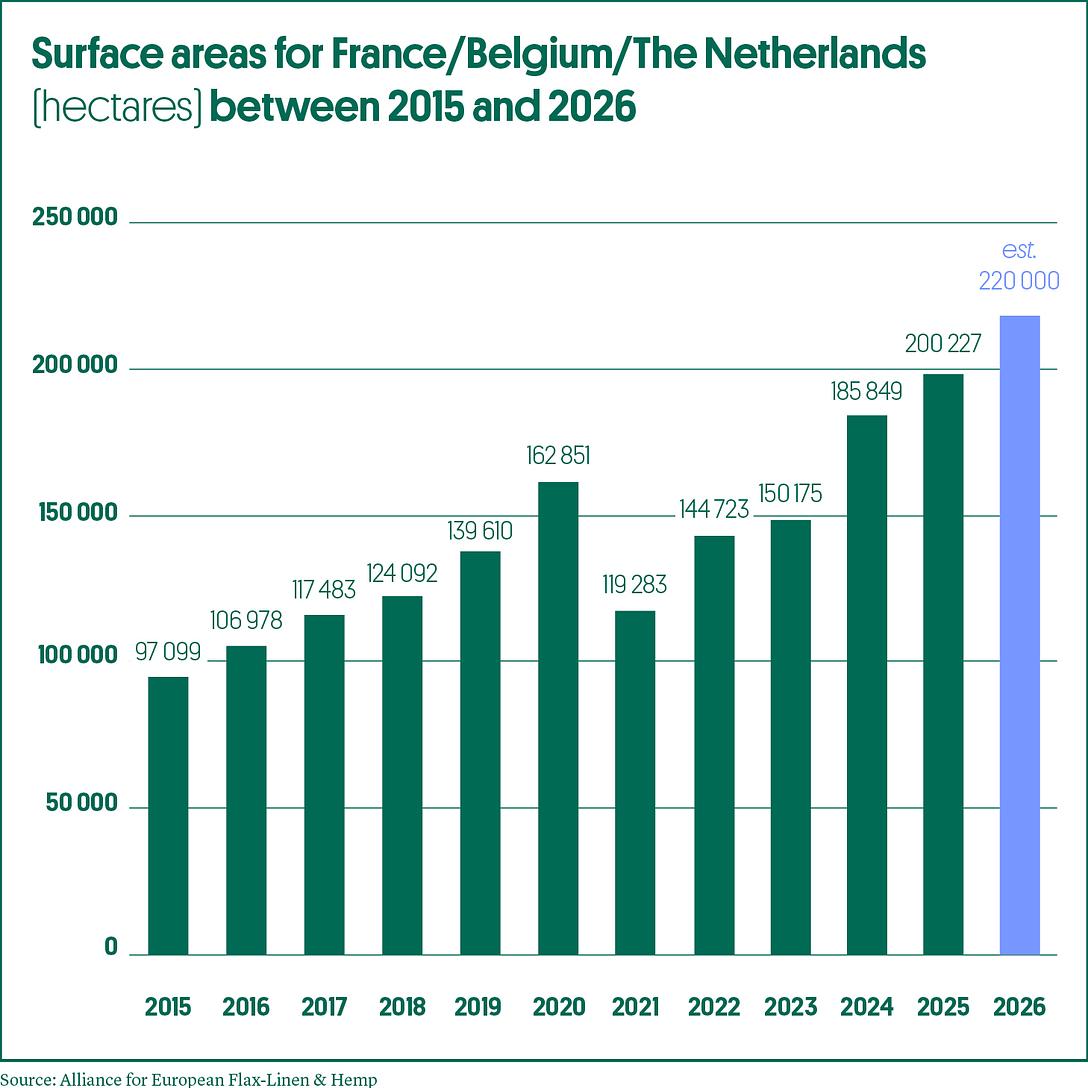

- According to estimations from the Flax-Linen and Hemp Economic Observatory, the Masters of FLAX FIBRE™ surface areas for spring and winter Flax combined for 2026 in France, Belgium and the Netherlands will represent at least 220,000 hectares – with an additional 2000 hectares for the United Kingdom.

- This is a new record and significantly higher than the previous 200,000-hectare record in 2025. The exact surface area will be known at the end of the spring when all agricultural administrative declarations have been submitted. A more precise estimate of the surface areas and an initial estimate of straw yields will be the subject of our next quarterly report.

A few words regarding the current situation on the fibre market for Masters of Flax FIBRE™

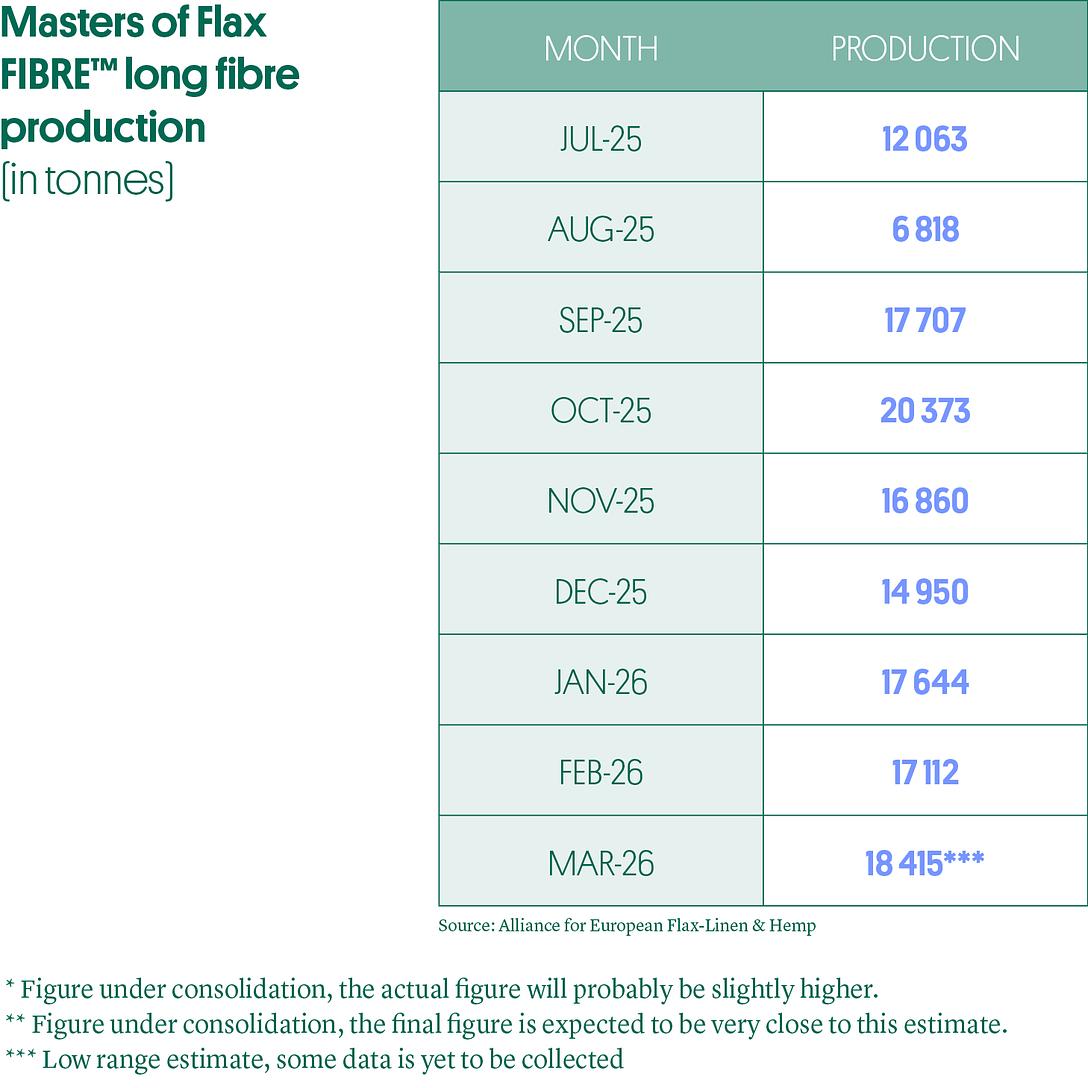

- The yields for the 2025 harvest were between 5.3 and 6.0 tonnes of straw per hectare, for spring and winter Flax respectively (exclusively for France) and an average of 1.0 tonnes of long fibres, following an excellent harvest in 2024. As a result,European scutching mills have been producing volumes of long fibres ranging from 15,000 to 20,000 tonnes per month since the beginning of the scutching season.

- Between July 2025 (the beginning of the scutching season) and March 2026 (the most recent figures available), European scutching mills have produced at least* 142,000 tonnes of Masters of Flax FIBRE™ certified long fibres. That represents an increase of 27% compared to the period between July 2024 and March 2025.

- The average price of Masters of Flax FIBRE™ long fibres was 5.89€/kg** in March 2026, for all qualities and regions of the EU combined. This marks a continuation of the gradual rise in prices since the beginning of 2026 – prices increased by 7.7% in the first quarter of 2026 – following a cap in the fall of 2025.

January 30, 2026 - Information release Q1 2026

Masters of Flax Fibre™ long fibres in 2026: Increase in growing area & continued dynamic supply

- As noted in the 19 December 2025 communication from the Alliance’s Flax-Linen and Hemp Economic Observatory, scutching mills in France, Belgium and the Netherlands are maintaining high production levels. This is explained by high yields in 2024 and 2025, which are now being processed by scutching lines, and recent industrial investments in Western Europe – 19 new scutching lines within a decade and numerous replacements of older lines – with the aim of developing capacity and market responsiveness.

- From September to December 2025, long fibre production was estimated at 70,000 tonnes, versus 50,000 tonnes during the same period in 2024, when scutching relied in part on the mediocre 2023 harvest. Over the course of the year, 2025 (with a production level of 190,000 tonnes) is both a record and a significant rebound from 2024 (116,000 tonnes).

- The outlook announced in our previous communication for the first half of 2026 remains unchanged: monthly production will be high, approaching, if not quite reaching, the 20,000-tonne mark between January and March 2026. From April to June 2026, the high pace should continue, with Western European scutching mills producing 17,000 to19,000 tonnes per month.

- The price of Masters of FLAX FIBRE™ long fibre: an upward trend After a rapid decrease in late 2024, bringing the average price per kilogram down from €9.00 in March 2024 to €3.33 in January 2025, the average price of Masters of FLAX FIBRE™ has risen gradually. In December 2025 – the latest available figure – the average price reached €5.49, a figure pending final consolidation, representing a 37% increase over a year. It should be noted that the context for this increase is radically different from 2023/2024, a time marked by a shortage of long fibre supply. Conversely, the current period is characterised by a record level of supply, also accompanied by very high demand, with an estimate of 185,000 tonnes – currently being consolidated – of long fibres sold over the year 2025.

- 2026 Masters of FLAX FIBRE™ Harvest Outlook The 2026 growing area is not yet known, as the sowing period for spring flax has not yet begun. Nonetheless, forecasts from national producer organisations, and significant figures from winter flax – between 55,000 and 60,000 hectares sown in late 2025 for the 2026 harvest, compared with 30,000 hectares the previous winter – point to a significant increase this year. Our estimates converge around a total of 220,000 hectares for 2026, compared with 200,000 hectares in 2025.

This would be the third consecutive year that the growing area record is broken. By way of comparison, in 2015, the growing area in Western Europe had not yet reached 100,000 hectares.

A more precise trend covering all growing areas will be published in the next quarterly communication in spring 2026.

Key Production Figures for European Flax Fibre - 2026

Key Production Figures for European Flax Fibre

-

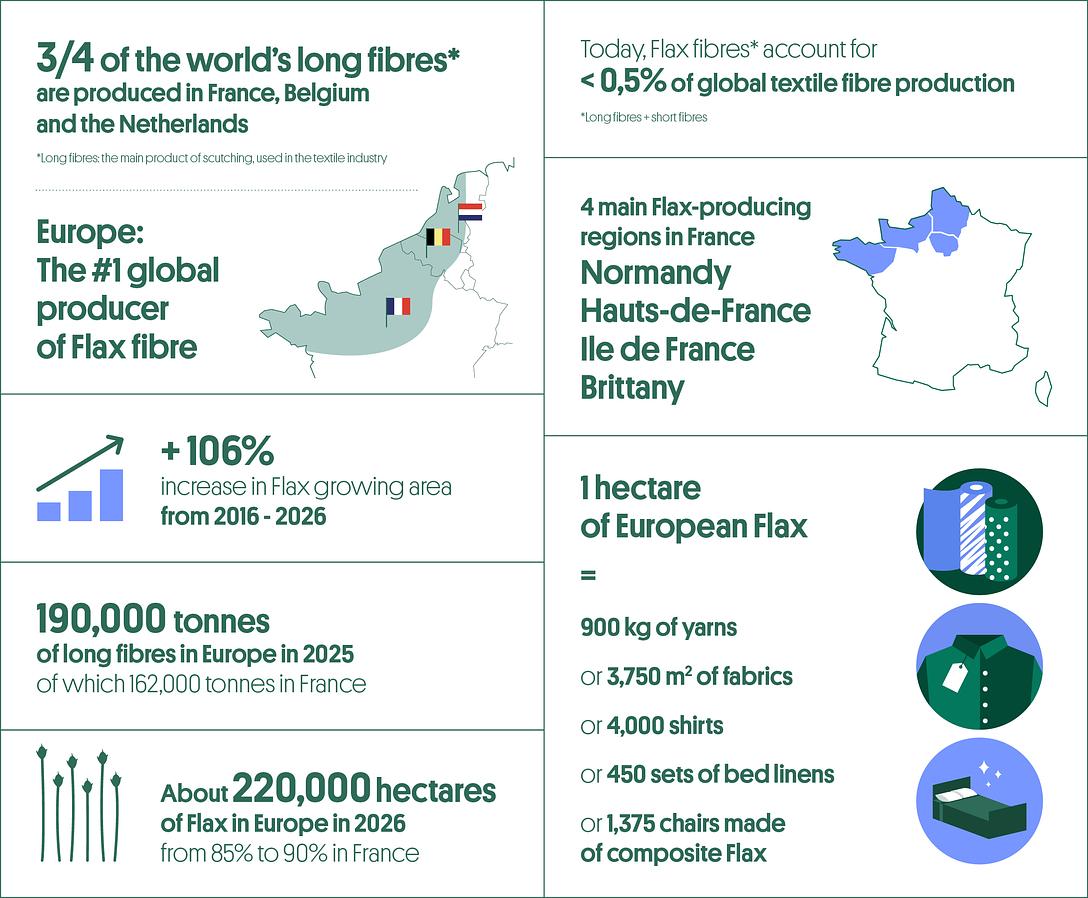

Europe is the world's leading producer of Flax fibre

- Three-quarters of the world’s long fibres (the main product of scutching, used in the textile industry) are produced in France, Belgium and the Nertherlands.

- Flax fibres (long fibres + short fibres) account for < 0.5% of global textile fibre production

- 4 main Flax-producing regions in France: Brittany, Normandy, Hauts-de-France and Ile-de-France.

- +106 % increase in flax area from 2016-2026

-

about 220,000 ha of Flax grown in Europe in 2026

(from 85% to 90% in France) - 190,000 tonnes of long fibres produced in Europe in 2025

-

1 hectare of European flax equivalent to:

- 900 kg of yarns

- or 3,750 m2 of fabrics

- or 4,000 shirts

- or 450 sets of bed linens

- or 1,375 chairs made of composite Flax

European Hemp Fibre production

Key figures for Hemp Fibre production

- Europe is the world's 2nd largest producer of Hemp with 36,500 ha of hemp for all uses in 2024.

- France is number 1 in Europe with around 24,600 ha of Hemp for all uses, including at least 1,650 ha for textile Hemp in 2025.

- China is the first global producer of Hemp, with 65,000 ha of Hemp for all uses including 27,000 ha of textile Hemp in 2024.

Previous Flax and Hemp information releases

The Linen and Hemp Economic Observatory regularly publishes information releases on the flax fibre market and the production of textile hemp:

2025 - Flax fibre market and production of textile hemp : See information release 2025

2024 - Flax fibre market and production of textile hemp :

See information release 2024

2023 - Flax fibre market and production of textile hemp :

See information release 2023