Flax-Linen and Hemp Economic Observatory - Figures 2023

Economic information on the flax fibre market and textile hemp production in 2023. Economic observatory collect, develop and share reliable data and information on European Flax and Hemp production.

Summary

European flax fibre market in 2023

September 12, 2023 - Information release

European flax - 2023 harvest estimates: towards a low production potential

A historically atypical and abnormally low production of flax fibre due to unfavorable climatic conditions throughout the plant's agricultural routes, from its sowing at the end of March to its harvest in June/July.

Flax, like many agricultural products, must deal with the consequences of climate change in France and around the world. The year 2022 was already the hottest ever recorded in France, with a difference of +2.7°C compared to the 1961-1990 average according to the Ministry of Ecological Transition. And most sources agree that 2023 will be the hottest on the planet.

Reminder of the first estimates for the 2023 flax harvest

During its communication on July 4, 2023 on the first estimates of the 2023 flax harvest, the Alliance for European Flax-Linen & Hemp provided a first estimate on the prospects at the start of the harvesting phase, taking into account the difficult climatic conditions which marked the spring and start of summer 2023.

At that date, the returns from farmers and scutchers fluctuated between yields between 3.5 and 5.5 tonnes of straw per hectare (6 to 7 tonnes of straw in a normal year) and a drop in the volumes of straw fiber estimated between 26% and 36%. However, the period of "retting" remained to pass - a natural process which extends from July to September during which precipitation, morning dew and the sun help the micro-organisms present in the soil to eliminate the pectose which welds the tex le fibres to the woody part of the stem.

Feedback from the field updated as of September 12, 2023

The retting period also experienced a generally unfavorable climatic context, with varia ons depending on the different growing zones. A relatively rainy summer in the northern part of France, Belgium and the Netherlands did not provide the optimal humidity/heat balance maximizing the potential in volume and length of fibres.

Concretely, this excessive rainfall in relation to the volumes of straw did not allow efficient retting.

From 6% to 12% of surfaces cannot be harvested. And, in the same area, not all plots have suffered the same climatic hazards and damage.

Flax : Straw yield and fiber yield

On most of the 147,000 hectares of the flax growing area, the straw yield should tend towards the lower estimate initially announced with a range of 2 tonnes to 5 tonnes of straw per hectare. The majority trend oscillates between 3.5 tonnes and 4 tonnes of straw per hectare.

Even if it is still necessary to remain cautious - estimates are still in progress - spring flax having suffered bad climatic conditions will have a yield of long fibers probably between 12% and 15%, a rather low performance, i.e. a yield of long fiber of 400kg to 500kg per hectare on the majority of plots. This would therefore represent half the potential in volume than the 2022 harvest.

Winter flax areas benefited from more favorable climatic conditions, and will show higher yields, of the order of 6.5 to 7.5 tonnes of straw per hectare. These areas, estimated in 2023 between 10,000 and 11,000 hectares, have doubled compared to 2022.

Forecast of the situation on the final market

As indicated in the July 2023 communication, the supply for the spring/summer 2024 season will be little impacted, this being supplied by yarn and fabric resulting from the assembly of different batches of fibers from previous years. The level of straw carried over into scutching* and therefore the production capacity in the coming months is the subject of ongoing estimates.

However, price tension is likely to continue with constant demand for linen in a context of increasing global demand for natural fibers.

July 4, 2023 - Information release

Initial estimate for the 2023 flax harvest

Temperatures above seasonal averages and very low precipitation

Weather conditions in recent weeks have had an impact on the initial outlook for the 2023 flax harvest, for which pulling has just begun.

The growing of flax, a technical crop with a short growing season, had already been disrupted this year by a particularly long sowing period, lasting from March to beginning of May (normally until mid-April). Alternating periods of dry spells and intense rainfall hampered early agricultural work that is so crucial for flax.

With an estimated increase of +2% compared with 2022, increasing total flax hectares to 147,000, French, Belgian and Dutch farmers are expressing their confidence in the market.

Initial feedback from farmers and scutchers on the ground at the start of the harvest

- The diversity of flax qualities will generally be preserved, and not all territories faced the same constraints. Nevertheless, initial estimates suggest that flax is shorter than normal.

- For 2023, yields varied between 3,5 and 5.5 tons of straw per hectare (6-7 tons of straw in normal years) with peaks of up to 7 tonnes for the very best plots. Under normal retting conditions, this would lead to an estimated 26%-36% drop in fibre volumes.

- During the current scutching cycle, between July 2022 and April 2023 (latest available data), long fibre production has increased by 3.3%, up to 125,264 tons, compared with the same period during the previous season (July 2021-April 2022).

- This harvest will be scutched in autumn 2023 together with flax from the previous harvest. Monthly fibre production could drop in early 2024, and an estimate will be prepared in October 2023.

The flax industry anticipates to adapt to new climatic conditions

An industry that anticipates and adapts to new climate conditions with the possibility of long-term changes to weather conditions: both temperatures and climate hazards.

- Winter flax, which has existed in the industry for twenty years, and which was originally developed to meet rising market demand, occupies 10,000-11,000 hectares in 2023, or twice the area compared with the previous year.

- The European industry was able to maintain its independence with respect to varieties, and flax breeders - French (2) and Dutch (2) companies - are innovating with new varieties to better address climate challenges.

- Arvalis institute, in charge of R&D in growing practices, has been working since 2019 on applied research known as BreedFlax to adapt flax to environmental changes and in the medium term aim for genetic improvement.

Consequences for the end market and retailers

The supply for the spring/summer 2024 season - still underway - will be little affected by a potential deficit in flax fibre production caused by the 2023 harvest. Fibres from this harvest will only be extracted once the agricultural cycle is complete (pulling and then retting in the field) and the flax has been sent to scutching mills, i.e., in autumn 2023.

- The spring/summer 2024 collections contain yarn and fabric made with different batches of fibres from several years.

- For 2024, the industry is already anticipating a significant increase in winter flax areas in addition to an increase in spring flax as well as an adaptation to scutching to smooth out the impact of the 2023 harvest.

European Flax™** certified long fibre is maintaining its leadership, accounting for 3/4 of the global offering of long fibres despite challenges facing the industry in recent years: the COVID crisis in 2020 (production interrupted for six weeks to comply with hygiene measures), weather events in 2021, the Russian-Ukrainian conflict and 2022 rise in energy prices, etc.

Permanently high flax prices

- With a demand for natural fibres on the rise and production capacity increasing more slowly, we observe a conjunctural pressure on the flax market (over-the-counter market).

- It has for consequences historically high and volatile prices. A tension that should last several more months.

Dialogue between the flax industry and the market

- A specificity of the flax sector which requires pursuing a rapprochement with the brands to ensure a dialogue between the end market and the sector to better anticipate needs.

- Flax penetrates all market segments, with however a natural positioning and prospects for more market growth in the premium and high-end markets.

Those positioning and strategy are already being deployed by the Alliance for European Flax-Linen and Hemp as part of its operational action plan with brands and retailers.

Key production figures for Flax fibre

-

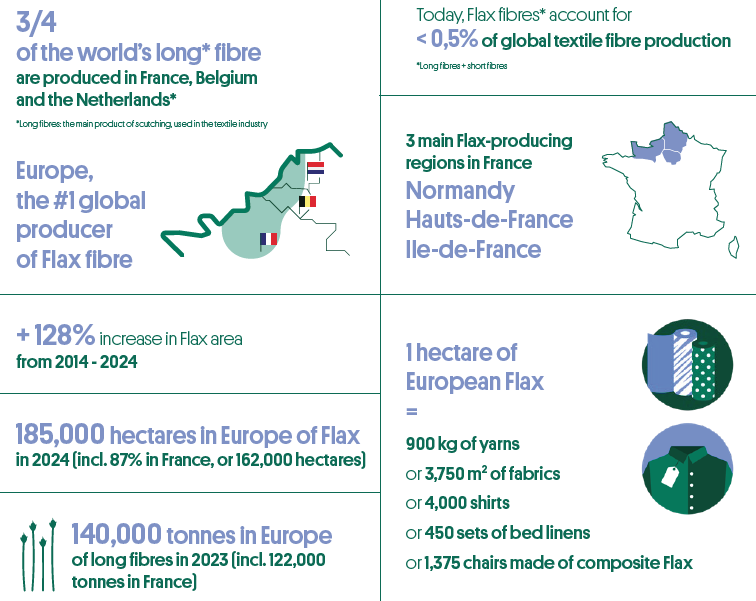

Europe is the world's leading producer of Flax fibre

Three-quarters of long fibres (the main product of scutching, used in the textile industry) globally are produced in France, Belgium and the Nertherlands. - +133 % in Flax growing area from 2010-2020

- 150,000 ha of Flax grown in Europe in 2023 (including 87% in France : 131,000 ha)

-

152,000 tonnes of long fibres produced in 2022

(including 125,000 tonnes in France)

- Flax fibres (long fibres + short fibres) account < 0.5% of global textile fibre production

-

3 main Flax-producing regions in France : Normandy, Hauts-de-France et Ile-de-France.

- In 2023, these 3 regions represented 80% of the European cultivated area, or 131, 000 ha of flax.

- In 2022, they produced 125,000 tonnes of long fibres

*Scutching is the process whereby the components of flax straw are separated out: short fibres, long fibres, shives, seeds, through mechanical crushing and threshing. This term also refers to the industrial facility where this operation is conducted.

**Fibre used by Northwestern European scutchers is European FlaxTM certified, guaranteeing a plant fibre from agriculture that is eco-friendly, irrigation-free barring exceptional circumstances, and GMO-free.

European hemp fibre production

Key figures for Hemp Fibre production

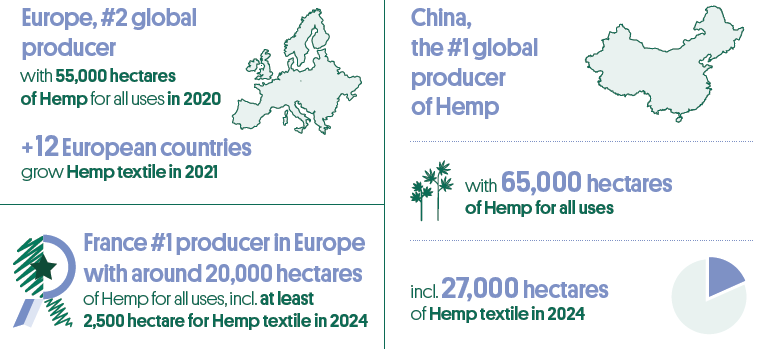

- Europe is the world's 2nd largest producer of Hemp with 55,000 ha of hemp for all uses in 2020

- More than 12 countries in the European Union growing textile Hemp in 2021

- France is the first producer in Europe with 21,000 ha of Hemp for all uses, including approximatively 10% for textile Hemp in 2022.

- China is the first global producer of Hemp, with 65,000 ha of Hemp for all uses including 12,000 ha of textile Hemp in 2021

Previous flax and hemp information releases

The Alliance provides regularly information releases on developments in the flax fiber market and textile hemp production:

2025 - Flax fibre market and production of textile hemp :See information release 2025

2024 - Flax fibre market and production of textile hemp :See information release 2024